People are always interested in investing but are doubtful where to start. Proper and long-term investment planning needs a range of financial advice and strategies in place to be successful.

A Good Money Management System is Like Getting Your Plumbing Right

If the tap you have leaks, but your normal usage hasn’t changed, you’ll use more water overall, with the excess literally going down the drain.

Well it’s the same for your finances and by simply avoiding the waste, you can improve and potentially dramatically improve your overall saving capacity. All while having little or no impact on your lifestyle.

This is part four of a five part blog series in which we will teach you to think like a business owner, by looking at the main ways money leaks from your savings, that can be fixed and then saved for your benefit. These are:

- Reduce your spending with a budget and save

- Legally reducing the tax that you pay

- Managing Debt Costs – By getting the structuring right

- Spending money that makes money with an investment plan

- Protecting your ability to earn income, with insurance

Spending Money That Makes Money Through Investment Planning

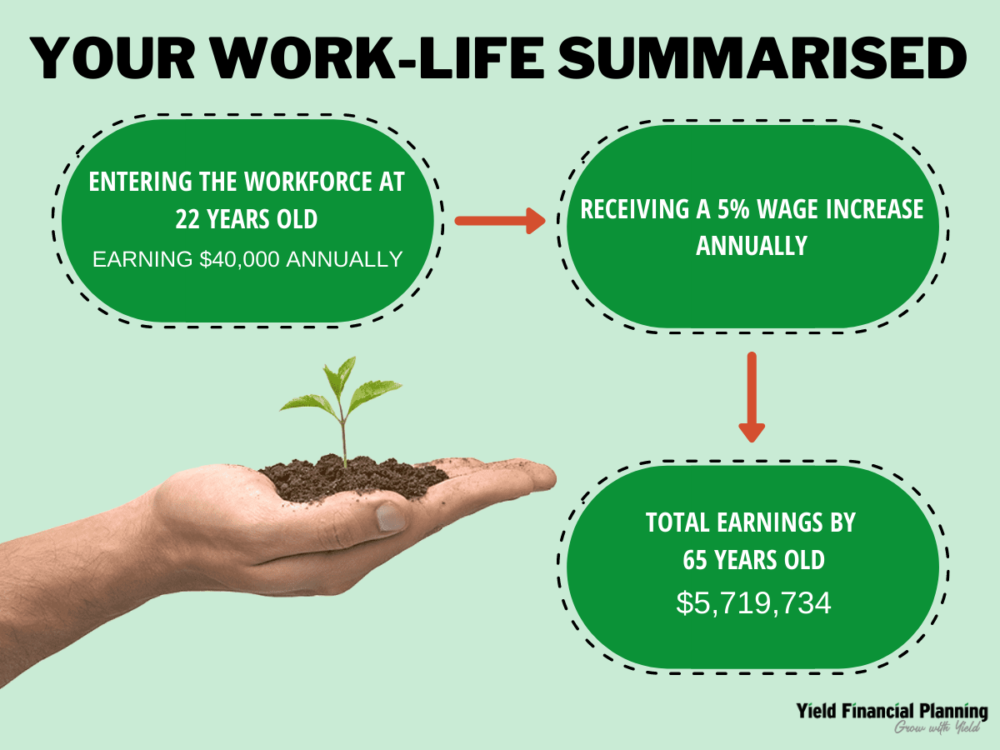

It is highly likely that the biggest financial asset you will have in your lifetime is the income you earn from your employment.

To illustrate this, if you entered the full time workforce at 22, earning a start wage of $40,000 and received just a 5% increase annually, you will earn $5,719,734 by the time you are 65.

It is therefore what you do with your earning capacity, while you are earning it, that will determine how long and how hard you have to work to achieve your desired lifestyle now and in retirement with your investment plan.

In this blog series, we have already explored strategies to budget and save; minimise tax; and pay down debt faster.

What we have therefore shown you in our previous articles, are investment planning opportunities to free up some of your cashflow and capital, which you can invest towards your ideal lifestyle in the future.

Thinking About Wealth Creation, Like a Business Owner

Successful business owners will endeavour to break down their short-term working capital requirements, from their long-term investment planning requirements. An example of this is purchasing equipment, to support business growth and create an investment return for the future.

For you, this is akin to identifying what you need to retain as a float, to cover your more immediate lifestyle needs, along with some reserves for short-term savings goals like holidays. Then to invest what you have left over, into investment planning opportunities where you can create wealth effectively.

The reality for most people, however, is that they are not adequately educated on the investment planning opportunities that exist and this naturally lends itself to fear of making a mistake. This investment planning inertia is what leads to most people either having less accrued wealth to rely on in retirement or being forced to work longer or harder to make it up.

How to Invest Savings and Capital?

When you are considering your investment planning strategies, it is important to define what capital you have available for investment planning and what ongoing saving capacity you have available for future investment too.

I would suggest you start by defining the accrued capital you have to work with, which will either be:

- Money you have saved in a bank account

- Investments you own currently

- Equity available in your home or other property you may own

- Investments you can make that can be used as collateral for an investment loan, such as a property or shares.

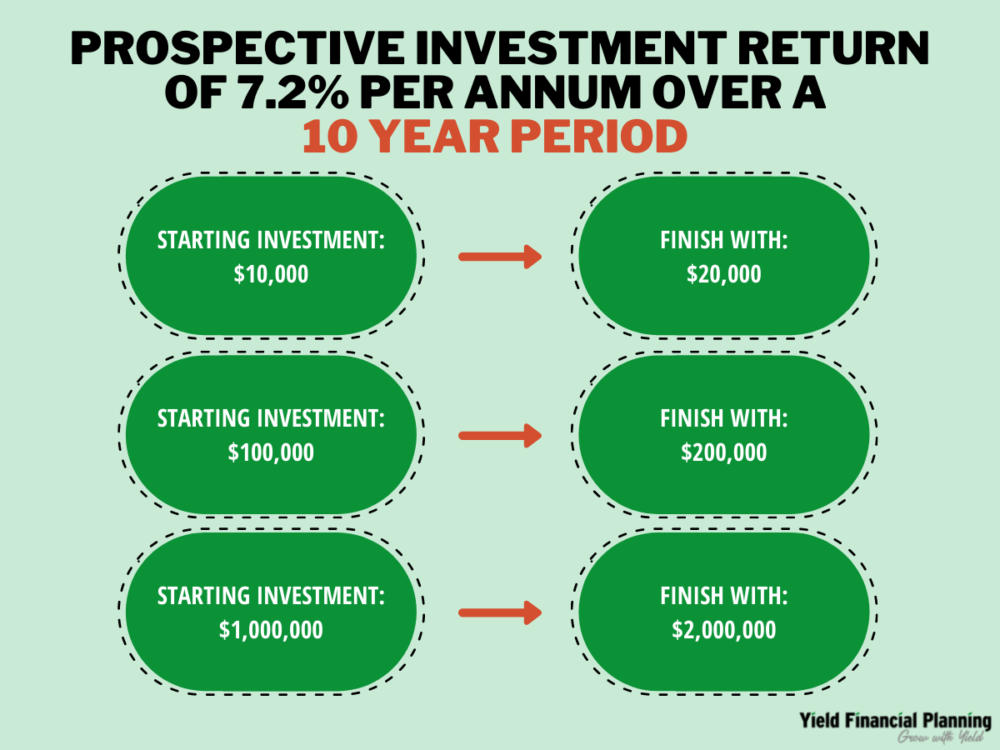

By planning for investment of your available capital first, you will give yourself an opportunity to make a larger investment to start with. This in turn can result in more compound growth over time.

Compound growth is very important when it comes to investment planning and to illustrate this simply, let’s assume a prospective investment return of 7.2% p.a. over a 10 year period. I use this particular rate of return and time period, because it is the factor that doubles money.

This means if you were to invest $10,000, you would have an investment return of $10,000, giving you a total of $20,000.

Time is therefore one of the most valuable commodities to effective investment planning. Like a business owner that makes an investment plan for the future, a successful investor will think about investment planning in years, rather than days or months.

How to Develop an Investment Plan Using Your Savings Capacity?

Once you have defined your initial investment planning strategy, you should assess and review how you use your surplus saving capacity as part of your larger investment plan.

How you choose to use this, will depend on a number of factors, including:

- How much debt do you have?

- Your personal risk profile

- How well diversified you are

- How long you have to invest for and in particular how close to retirement you are

Each of these factors will help you determine if you should be contributing your surplus into an ongoing investment planning strategy, where you essentially top up your existing investment plan, focus on debt consolidation, or a combination of these things.

The benefit of contributing regularly to an investment is that it removes a lot of market timing risk. Regular investment planning by its definition will mean that you are investing at low points in your chosen investments, as well as while they are growing, smoothing out your overall investment return and volatility.

Regular investment planning also means that your savings will benefit from compound growth as well. A great example of watching how this ongoing saving positively results in compound growth is to track your super performance over a long period of time. What this should show you is the overall upwards momentum of growth, getting exponentially larger as the balance has grown.

What are The Best Investment Planning Options?

Firstly, you should identify what you are comfortable investing into. Usually this means you are either a share market or a property person.

At Yield, we are big advocates for understanding what your current investment plan is. No matter how scripted or unscripted it is right now. By defining your current investment plan, it demonstrates how you feel comfortable using your money and forms a baseline for you to build wealth from.

With this said, the best approach to developing your investment plan overall is to diversify. Especially over the longer term, as you begin to rely on your investment portfolio and management to fund your retirement income needs.

Investment Planning For Your Risk Profile

True investment planning success is achieved when your investment plans are working for you. The aim is to support the lifestyle you love to lead now and that you want for yourself in the future.

If you overextend yourself or invest outside of your risk profile, you can very quickly find yourself in a position where you are essentially working for your investment strategy, instead of it working for you.

We see this too often, particularly amongst property investors that borrow heavily. Even if over time your investment plan eventually works out, in hindsight, investors in this position have often told us that the ends do not justify the means.

Investing within your risk profile is therefore as much about finding lifestyle balance as it is about finding a comfort level with volatility that the investments may have along the way.

Yield Financial Planning is Here to Help

Spending money to make money is the most fundamental building block to successful investment planning. A strategy to invest your available capital, including where to borrow to invest, and then using your surplus saving capacity to good effect is a way to help you build on your investment strategy and reduce your debt over time.

At Yield, we are investment planning experts. Please feel free to contact us for a strategy health check or to discuss your current plan for the future.