While we’ve shown that debt can be a great part of your strategy, it is also a drain on your cash flow and so needs to be managed wisely.

You will be pleased to know there are a variety of steps you can take to formulate a clear and SMART debt reduction plan, which I’ve summarised for you below and throughout this section, we’ll discuss each in more detail:

- Develop a budget

- Payout your credit card in full every month

- Improve your interest rate

- Understand good and bad debt

- Optimise your loan structuring

- Asset sell down strategies

- Superannuation strategies

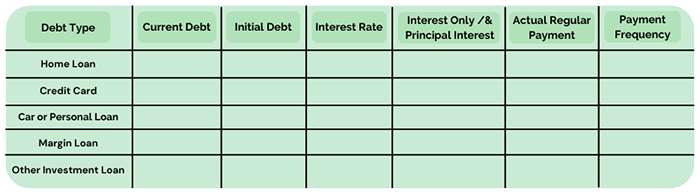

As a start though, below is a table for you to copy and populate. It includes what your current debts are, what level they started at, what interest rate you pay, whether your repayments are Interest only or Principal and Interest, what amount you physically pay, and in what frequency. This process will provide personal insights for you to reflect on throughout this section.

Now you’ve done this, how does it make you feel?

I ask because you are either going to like what you see or at least feel completely comfortable with it, because you have good savings habits, or you are going to be a bit worried about it, or possibly a bit embarrassed by it, because you know you have not managed your debt or saved the way you could have over the years.

Whatever you are feeling right now, is a great insight for you to think about, because good cash flow management is not only important with regards to how effectively you reduce your debt, but it is also a discipline that you will need to make your money last in retirement as well.

If you do not have good savings habits currently, then the most important thing that you should do is start with a budget to manage your spending and create a savings plan.

Why This is a Good Option

Very few people are suited to having debt in retirement and what I’ve found is that even those that have the risk tolerance for it, usually do not want or need the additional risk anyway, so formulating an effective debt reduction plan simply makes sense.

Determining what you can save, based on your current outgoings, is the most logical place to start because it dictates everything else. Once you are clear on this, overlaying some of the additional strategies I’ve touched on will make your money work harder overall.

I’ll explain a little further what each of the debt strategies noted are and how they can really complement your savings efforts.

Payout Your Credit Card in Full Each Month

One of the biggest debt traps you can fall into is leaving a residual balance on your credit card. We see it surprisingly often when people have other means of reducing their debt to zero each month. As a rule credit card debt has a higher interest rate than any other debt and the expense is typically not tax-deductible. Given this, even if you need to dip into another loan like your home loan – If you can save on interest then you are paying less to the bank and keep more working for you!

Improve Your Interest Rate

One simple step to a smart debt reduction plan is to refinance debt to a cheaper interest rate and you should consider reviewing this ongoing, because lower interest = more money in your pocket for principal debt reduction. Banks and other financial institutions will usually negotiate with you too, so it is worth your while to shop around.

Good Debt vs Bad Debt

A key principle of a good debt reduction plan is to group the debt you have into Investment debt and Personal debt. This means first that you know the difference and it also means that you have your investment debt completely separate from your personal debt.

Is most of your debt Investment or Personal?

The reason to clarify is that interest on investment debt is tax-deductible against your taxable income at tax time whereas your personal debt is not. What this means to you, is that the interest rate is only one consideration and in reality, it is usually more beneficial for you to keep investment debt on an interest only basis, and focus on reducing your personal debt first. Even when the interest rate on your personal debt is lower. It’s important to do the numbers though. Try working yours out now:

Personal debt cost p.a. = Interest rate x total debt

Investment debt cost p.a. = Interest rate x total debt – Personal marginal tax rate

Optimise Your Loan Structuring

Hopefully, you have a diligent lending adviser who is all over this for you, but if the mere mention of loan structure does not jump out at you as something you have well organised, then it really is important!

Offset accounts, interest-only loans, equity buffers, differentiated loan accounts. Do you know what you have and if you do, do you know what it is all for and how it is helping you?

Offset accounts sit alongside your loan and do what they sound like. They offset your debt, as if you have repaid it, but the difference is that you can preserve the debt you have in its original form while maintaining ready access to the cash. Remembering what we have just covered about good debt and bad debt, this is especially important when you only have investment debt or ‘good debt’ left. It means that if you accumulate savings of say $50,000 in your offset account and then need to buy a non-deductible item, such as a car, you can redraw the cost of the car from your offset and still claim the interest as tax deductible. This is because the original purpose of the debt was for investment.

Offsets also = flexibility, regardless of whether you are offsetting good or bad debt and I could go into more detail here, but I won’t, other than to say that offsets may well have a place in you maximising your debt reduction efforts.

Interest-only loans are again as they sound. You only pay interest. You are not obliged to make principal repayments on a loan that is interest only and it is generally the best, most flexible way for you to manage your debt. If you reflect on your current loans – do you pay ‘principal and interest’ or just interest?

As part of your loan structure, it is typically ideal to have redraw available. Having higher loan limits than you presently need can seem counterintuitive to the objective of extinguishing all of your debt, but there are a variety of reasons it can make sense. Do you have re-draw available in your current home loan and if so, how much?

Re-draw = flexibility and in essence, you become your own banker. The more you have, the more flexibility you have to manage your personal situation and needs. Say you want to tap into equity to invest for example. Rather than needing to approach the bank, you can simply redraw on your loan. Another advantage can be that by taking out a higher loan in the first place with a bank, even if it is more than you need, it can result in the bank you are with giving you a better interest rate.

Lastly, you need to have your debt grouped into good and bad debt. It can even make sense to have multiple investment accounts. It keeps what is tax-deductible clear at tax time and gives your debt strategy focus.

Asset Sell Down Strategies

Diverting cash flow to an investment, like what we’ve outlined in strategy 3, naturally means you have less money to put straight on your home loan, but it can still make sense. Strategy 3 highlights how this can work and if you do decide to go down this road, then tying it back to your debt reduction plan can be a good option.

Reflect on your asset position for a moment. What investments do you currently have earmarked for your retirement?

Selling them down once you have retired, in a financial year where your taxable income is low, will reduce your overall tax payable and therefore maximise the amount that you have to pay down debt. Approaching this strategy with foresight, projecting assumed rates of growth and income for your investment, will give you some degree of confidence in how much impact your investments will have on your overall debt reduction, however also keep in mind that the end goal is to have enough capital to meet your income needs, net of debt, so reducing your debt is only part of the puzzle, of meeting your retirement needs.

Superannuation Strategies

So here we are back talking about super again. I’ve already highlighted in some detail why super is tax effective, and it is due to the tax savings that maximising super contributions over debt reduction can make the most sense.

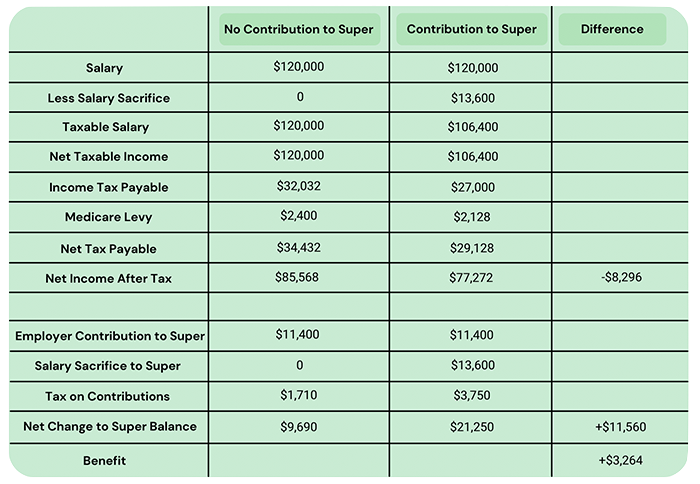

To illustrate how super can work as a strategy for reducing debt, take a look at this example:

- Say you earn $120,000 per annum.

- Current employer super contributions of 10% equals $12,000 p.a.

- The Concessional contribution cap is $27,500 so you can contribute a further $15,500 before you reach your contribution limit for the financial year.

One option and possibly what you are doing currently is simply putting this saving into your home loan, being an extra payment of $691 p.m. Another option is that you maximise your super contribution

The following table shows how these two options might look like, in a very simple form:

One question here is going to be whether using the $8,296 to reduce your loan or investing the $11,560 in super is going to be more beneficial long term.

Aside from being $3,264 better off within the year, it is also worth considering whether you might be able to outperform the interest saved on the loan had you opted to do that.

If your loan interest rate was 4.5% p.a., a payment of $8,296 would save you $373.32 in interest a year. If instead the $11,560 was in super, in order to earn $373.32 after 15% tax, you’d need to earn $439.20 before tax. This equates to a rate of return of 3.80% on the $11,560 deposited and having previously discussed the benefits of investing long term in option 3, one would think a return at that rate should be achievable.

If these numbers are making your eyes bleed a bit, I do get it, but if this is the case, take the time to read it over a few times to really digest it, because this reflects the key value of how this strategy can work for your debt reduction.

It’s important to keep in mind also, that with the benefit of compounding, your superannuation can be supercharged so that at retirement, once you are able to access your super, you could consider withdrawing the funds tax-free to pay down the debt.

When preparing financial plans for our clients, we include comprehensive cash flow planning that incorporates all of these strategies where applicable towards the common objective of being debt-free in retirement. We also offer an integrated mortgage broking service, which we feel we are best placed to provide for our clients for three reasons:

- We make it simple because we already have so much of your personal data

- We are helping you create your strategy and including your debt strategy in this is integral

- We are regularly meeting to review your position and debt is always an important part of the conversation

What Scenario and Risk Profile/Person Does This Make Sense For?

For anyone who has debt, a focused debt reduction strategy should be a consideration for retirement planning.

Regularly reviewing your interest rates to market and refinancing where appropriate; Recapitalising your loans to lower interest rates, like in the example of paying off a credit card; and focusing on the loans that have the highest NET cost to you, are all low-risk options of keeping your interest outgoings to a minimum and therefore increasing the amount of savings capacity you have to further reduce your loan principal.

Organising your loan structure well, to ensure you can quickly and easily redraw on your loans, including interest-only loans, with offset accounts typically reduces your risk, by increasing your flexibility to access funds.

With this said, you may not find this option suitable if you feel you cannot be disciplined enough not to draw down on the equity and spending what is available to you on unnecessary expenses. If this sounds like it is a risk for you, then you are probably more suited to a more structured principal and interest arrangement.

Separating your good debt and bad debt is suitable for all risk profiles because it can only improve your cash flow, thereby freeing up cash flow that you can use to reduce your loan principal.

Additional super contributions do have a higher degree of risk than simply paying down debt, because you will likely have a fairly large exposure to growth investments, including shares and property, but given the tax benefits, it remains a relatively low-risk strategy.

If you were particularly conservative, you could reduce your risk further, by quartering out your additional contributions to a very low-risk strategy of cash and fixed interest, so that volatility on these funds is kept to a minimum.

Finally, tapping into home equity to invest, with a view to selling an asset for debt reduction, is a high growth strategy and at the higher end of the risk tree. However, given the time frame of ten years and depending on how diversified you are amongst other things, you can manage some of this risk. Refer back to the risk profile section of Strategy 3, to read more about this option.

This blog is an excerpt from our “Top 5 Pre Retirement Strategies” eBook, which is available for download below.

Free: Top 5 Pre-Retirement Strategies

Please enter your email address to be able to download this e-book.