Let me start by saying, I love super for retirement and this is why I’ve put it as Strategy 1. Depending on your life stage, you will have a different set of values and strategies on how to grow your super balance.

Yield acts as your guide on how to best grow your super balance in the most effective way possible based on your goals for retirement.

The most significant thing to love about your super is that it offers THE BEST tax structure available in Australia.

If I’m already losing you because I’ve raised the ‘t’ word, I want you to fight the urge to switch off! Tax is a straight-out cost on your investment return and if you can pay less, without compromising your return, then you will achieve your goals sooner. Simple as that!

In my experience in asking what people’s biggest expense is, people usually say their home loan payments, but I’ve encountered very few people who will say that it is the tax that they pay.

I think that this is because in the most part we just accept that tax is, like death – unavoidable, and while that is true to an extent, there is a range of ways to legally manage and reduce your tax bill.

Super is one of these strategies, and it is there to be exploited. It is always an attractive consideration, but especially when you are getting closer to retirement.

To demonstrate, let’s look at some facts about super’s tax structure:

– When you put money in to grow your super balance;

– While it is in a super fund; and

– When you take money out of super.

When you put money away to grow your super balance

Are you employed at the moment?

If you are, then you currently enjoy super contributions from your employer at 10%, which was increased from 9.5% as of the 1st of July 2021. The Superannuation guarantee will continue to grow at a steady rate of 0.5% each passing year until it reaches 12% in 2025.

What’s more, the amount you are taxed on this money is, in all likelihood, lower than the tax that you pay on the personal income that hits your bank account.

If you earn less than $250,000 p.a., your super contributions will only be taxed at 15%.

This compares to upwards of 47%, depending on your personal income and any levies that might apply at the time.

Even if you earn more than $250,000 p.a., your contributions are taxed at a maximum of 30%, which is still a meaningful saving and this saving goes straight towards your retirement, instead of into the tax man’s pocket.

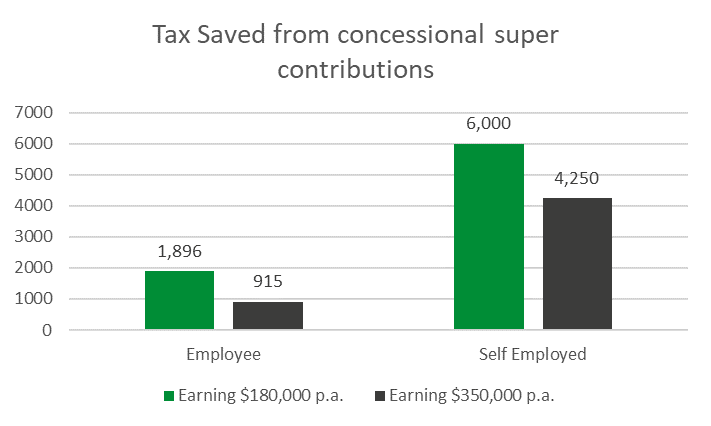

What the above graph shows, is the amount of tax you could save per annum by maximising your super contributions to the $27,500 concessional cap in the 2021-2022 financial year, set to take effect on the 1st of July 2021.

Whilst these figures may look small, implemented over the long-term could make a significant impact on your finances.

For example, $1,896 over ten years equals $18,960 which could fund an entire family holiday or a sizeable contribution to a home renovation.

Note under ‘employee’ it assumes you are already being paid mandatory super contributions from your employer, therefore reducing the amount you can salary sacrifice, while under ‘self-employed’ it assumes you were not contributing at all to begin with.

While the balance is growing in your super fund

Did you know that while you are working and contributing to super, your super’s investment earnings are taxed at between 10% – 15%.

This compares to your personal tax rate of up to 47% of funds were invested by you personally.

Again, it sounds attractive, right? Every dollar you save, by not paying as much tax means your money is helping to grow your super balance over time by ‘compounding’ faster, which is the aim of building wealth for your retirement.

But it gets better. When you are retired and over 60 years old you pay no tax on earnings.

This is literally a legal tax haven for retirees

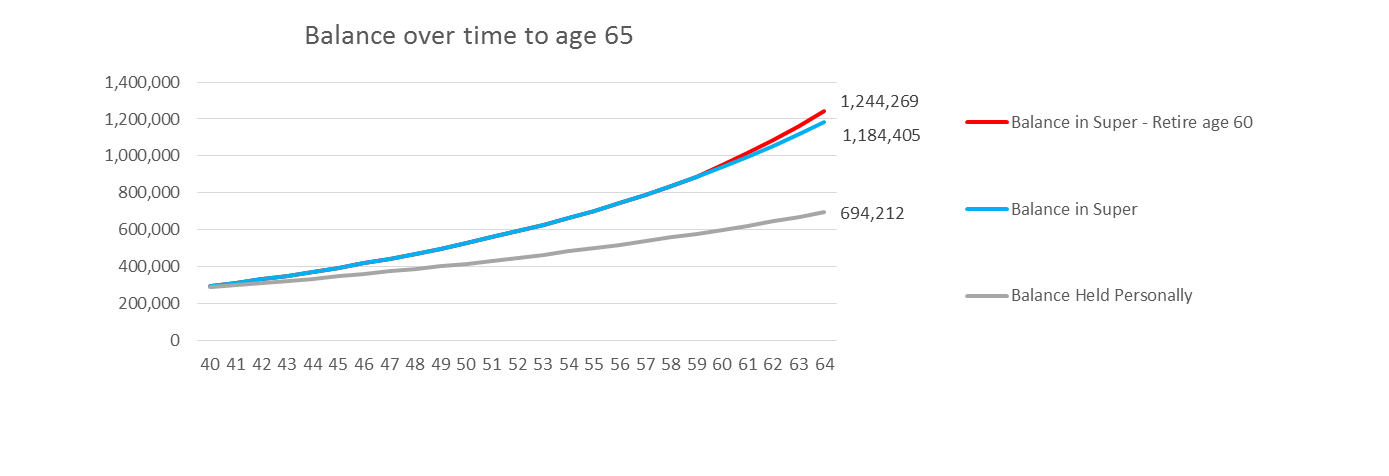

The following chart demonstrates how you could grow your super balance over time by looking at an average balance in super of a 40-year-old earning $200k p.a.

It assumes there are no contributions over the period and that tax is paid on all earnings each year.

Assumes a rate of return of 7% p.a. is used, super is taxed at 15% and personally held is taxed at 47%. Tax is applied to all earnings each year.

To explain what you are looking at in this graph further:

- The red line is the best outcome as can be seen and is a person that retires at age 60 and converts their super to pension. They benefit from 0% tax on earnings, to age 65.

- The blue line is money invested in super, with the tax concessions it provides.

- The grey line is money invested personally

The difference to the retiree at age 60, is around $600,000, with the end total for money invested in super, just below double the total invested outside super.

The benefit is purely due to the different tax rate applied, so having a financial plan applied to your tax structure could mean a significant increase in your super balance.

When you take money out of super

Once you reach 60 years of age and retire, super is so flexible that you could withdraw the whole lot on day one if you wanted.

The government has made it this flexible for people to withdraw, because really, why would you take money out of a tax-free environment?

I’m not saying there are not limited examples where it can make sense, but the incentive to keep it in is hard to argue with.

As you are considering retirement, I will hazard a guess that your income is probably at or near its highest point.

Your home loan is probably reduced significantly from when you first took it out. Your kids have either finished school or the end is in sight.

If any or all of this is true for you, then you likely have surplus cashflow you can consider investing for retirement and for the reasons outlined they should be high on the retirement agenda.

Put a focus first on making pre-tax ‘salary sacrifice’ contributions from your employer, ideally to the maximum, where appropriate.

Also, depending on what other investments you currently have outside of super and/or that you have successfully accumulated between now and retirement, consider the merit of transitioning your outside wealth into super.

After all, if it is possible to have all of your retirement wealth in a tax-free haven where you can potentially invest with the same flexibility as you can outside of super, why wouldn’t you want it in there?

The most common reasons and criticisms we hear for people not really embracing and investing in super is that the rules are convoluted and always changing or that it is boring and they have no interest in it.

On the later point, if you feel this way, hopefully what you have read has piqued your interest enough to realise that it is a structure you should not ignore. If that’s the case, please feel free to contact us so that we can help guide you further.

On the first point, there is no escaping that super is complex, and that change is inevitable.

Especially when you consider that the total superannuation pie in Australia is such a large sum of money.

The current super value in Australia is $3 Trillion as of May 2021, and is expected to grow to $9.5 Trillion by 2035.

Given the enormity of these numbers, it’s easy to be cynical that the government of the day will continually look this over when preparing their annual budgets for ways to drive some extra tax revenue, because they will!

However, this is simply not a good enough reason to dismiss super.

The important thing is to stay alert but not alarmed. Stay abreast of the changes and move with them.

The more aware of change you are, the better prepared you are to plan for them and what you’ll notice too, is that not all change is bad.

The best way to be on top of and adaptable to these changes is having a financial planner whose job it is to adjust your financial structure to the new rules whilst still ensuring you are in the most optimal position possible.

I’ve been advising for over 15 years and what I’ve found is that change invariably has brought with it new opportunities.

As a last point, it is worth remembering that the rules and regulations that apply are there first and foremost to try and protect your money, so you can achieve a comfortable retirement.

What scenario and risk profile/person does Superannuation make sense for?

The great thing about super is that it is simply a tax structure. It is not the investment itself and this is a point I’ve found that a lot of people do not fully understand.

Yes, it is optimal for investing, but if you do not consider the tax benefits and structures of this, you are only using half of the benefits of the superannuation system.

How you invest your money inside super is entirely up to you and therefore how you choose to invest your super should be considerate of your own personal risk profile.

When choosing a super fund option that is right for you, you should consider how much involvement you want in the investment decisions.

There are very simple no-frill options available, like the industry funds, that offer basic investment options like Balanced or Growth and if you choose a basic fund, then it is simply important to know which investment option best fits your risk profile.

From there though, there are increasingly more sophisticated options that go right through to Self-Managed Super Funds (SMSF), which give you a large degree of flexibility to grow your super balance in a lot of the things you can personally, allowing you to create an investment strategy that is perfectly suited to you and your family’s needs.

If you would like to read more of our retirement income strategies and the steps we recommend and implement into our client’s financial plans, download below. Or, you can read the next step to taking control of super with a SMSF.